Understanding tax brackets is essential for managing your finances effectively. Many people mistakenly believe that being in a higher tax bracket means all their income is taxed at a higher rate. In reality, the U.S. tax system is progressive, meaning only the portion of your income that falls within each bracket is taxed at that rate.

By learning how tax brackets work, you can make smarter financial decisions, reduce your taxable income, and optimize your tax planning. Let’s break down tax brackets, how they impact you, and actionable strategies to lower your tax bill.

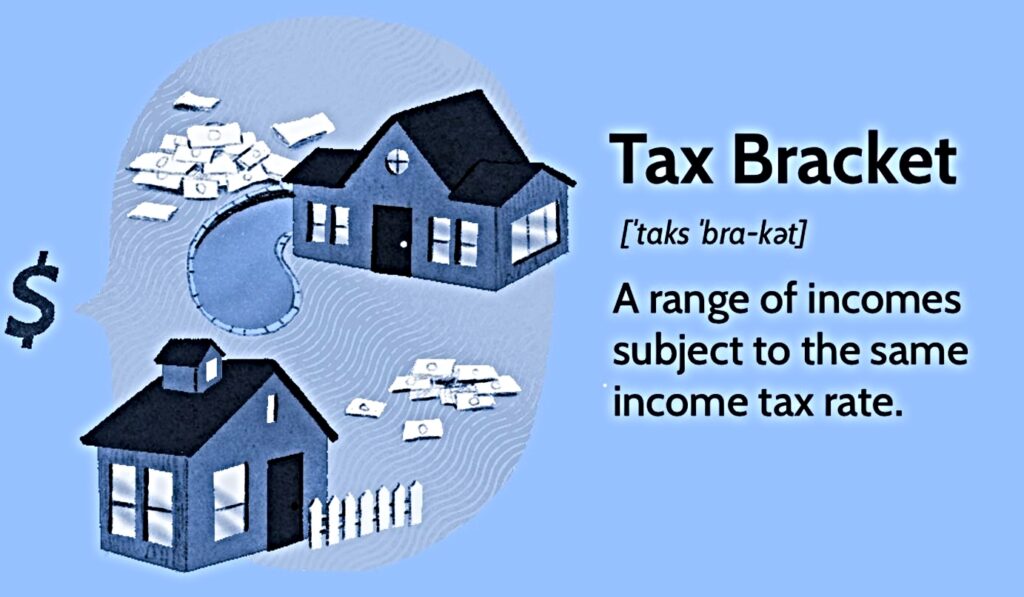

What Are Tax Brackets?

A tax bracket refers to the range of income taxed at a specific rate. The U.S. has a progressive tax system, meaning the more you earn, the higher the percentage of tax you pay on portions of your income. However, not all of your income is taxed at the highest rate—only the portion that falls within each bracket is subject to that rate.

The IRS adjusts tax brackets annually based on inflation. For 2024, the federal income tax brackets for single filers are:

| Taxable Income Range | Tax Rate |

|---|---|

| $0 – $11,000 | 10% |

| $11,001 – $44,725 | 12% |

| $44,726 – $95,375 | 22% |

| $95,376 – $182,100 | 24% |

| $182,101 – $231,250 | 32% |

| $231,251 – $578,125 | 35% |

| Over $578,125 | 37% |

For married couples filing jointly, the brackets are higher.

How Tax Brackets Affect You

Understanding how tax brackets impact your income is crucial for tax planning. Here’s what you need to know:

- Your entire income isn’t taxed at one rate.

- Example: If you earn $50,000, the first $11,000 is taxed at 10%, the next portion up to $44,725 is taxed at 12%, and the remaining portion up to $50,000 is taxed at 22%.

- Marginal vs. Effective Tax Rate:

- Marginal Tax Rate refers to the highest bracket your income falls into.

- Effective Tax Rate is the average rate you actually pay across all brackets.

- Impact on Take-Home Pay:

- Knowing your tax bracket helps you estimate how much of your paycheck goes to taxes and how much you take home.

Ways to Lower Your Taxable Income

Understanding tax brackets allows you to implement strategies to reduce your taxable income legally:

1. Maximize Tax Deductions

- Take advantage of the standard deduction ($14,600 for single filers in 2024, $29,200 for married couples).

- Itemize deductions if they exceed the standard deduction.

- Common deductions include:

- Mortgage interest

- Student loan interest

- Medical expenses exceeding 7.5% of your AGI

2. Contribute to Tax-Advantaged Accounts

- 401(k) & IRA Contributions: Reduce taxable income by contributing to retirement accounts.

- Health Savings Account (HSA): Contributions are tax-deductible and withdrawals for medical expenses are tax-free.

3. Use Tax Credits

- Unlike deductions, tax credits directly reduce the amount of tax you owe. Popular tax credits include:

- Earned Income Tax Credit (EITC)

- Child Tax Credit

- Lifetime Learning Credit

4. Harvest Capital Losses

- If you have investments, consider selling underperforming assets to offset taxable gains.

5. Adjust Your Withholding

- If you consistently owe taxes or get large refunds, adjusting your withholdings can help you keep more money in your paycheck throughout the year.

Common Misconceptions About Tax Brackets

Myth: Earning more money puts all my income in a higher tax bracket.

Fact: Only the portion of income that falls within a higher bracket is taxed at that rate.

Myth: Tax deductions and credits are the same.

Fact: Deductions reduce taxable income, while credits directly reduce the tax owed.

Myth: A tax refund means you paid exactly the right amount of taxes.

Fact: A refund often means you overpaid taxes throughout the year.

FAQs About Tax Brackets

Q: How do I determine my tax bracket?

A: Your tax bracket is based on your total taxable income after deductions. Use IRS tax tables or a tax calculator to find your bracket.

Q: Can I change my tax bracket?

A: While you can’t change tax brackets, you can lower taxable income using deductions and credits to remain in a lower bracket.

Q: Do state taxes have brackets too?

A: Yes, most states have their own tax brackets, though some have a flat tax rate instead of a progressive system.

Q: How often do tax brackets change?

A: The IRS adjusts tax brackets annually for inflation, and Congress may change tax rates through legislation.

Conclusion

Understanding tax brackets is key to making informed financial decisions. By knowing how your income is taxed, leveraging deductions and credits, and using strategic tax planning, you can keep more of your hard-earned money.

Want to learn more about optimizing your finances? Visit GetCashVibe for expert personal finance tips!